We all know saving money provides tremendous advantages to our bank accounts and finances. But did you know that having savings also boosts your mental health? We sometimes think of savings as something painful, especially in the present, but research reveals the future benefits of saving aren’t as distant as one might think.

A recent report of the household saving rate in the U.S. by the Bureau of Economic Analysis revealed a decrease in household savings to 4.80%. This is a significant drop from the all-time high of 32.00% in April 2020. More than one in four Americans have less than a thousand dollars in savings.

As we have seen, routine expenses have continued to grow over the last several years, and the chances of having more than a thousand dollars in unexpected expenses is much more likely now than just a few years ago. Saving is something many people struggle to do, but once it becomes a habit, you put yourself in a better position mentally as well as financially.

For many, lack of savings creates psychological distress, though we may not identify it as a significant cause of stress. However, when you consider the benefits of savings, you can see how the future return on your savings appears more quickly than anticipated.

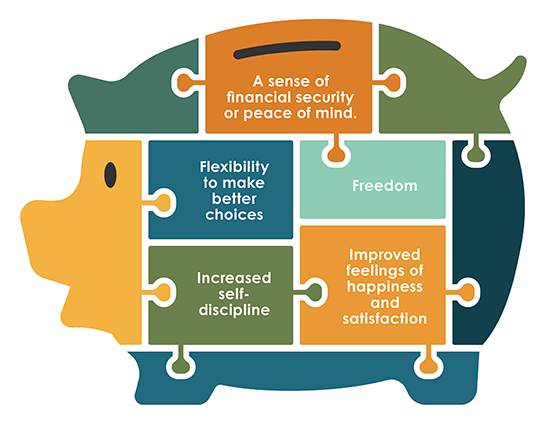

Consider just five of the numerous psychological benefits of setting money aside for the future.

1. A sense of financial security or peace of mind. If we are running paycheck to paycheck, living on the max of our income, it causes stress. A cushion to handle the unexpected provides us with some “breathing room.” A savings cushion brings peace of mind by providing a lifeline to grab if the unexpected does occur. While everyone with healthy savings doesn’t live stress-free, building a healthy cushion reduces the number of events to worry about because the margin gives you options. Having options brings peace of mind and keeps you from desperate decisions. Savings can be treated like a self-funded insurance policy upon which to draw when the unexpected happens.

2. Flexibility to make better choices. While a sense of security and peace of mind is primary, another benefit is the flexibility to make financial choices. When living on the edge of a budget, the loss of a job or an unexpected major expense can cause everything to come crashing down. This causes us to scramble to make ends meet, since we were flying without a safety net. However, with an adequate cushion in savings, you have time to look over your options and the flexibility to choose next steps. This ability to choose provides a psychological benefit for people. Studies show that people dreading an upcoming meeting with their boss feel more positive when they have a choice regarding some aspect of the meeting. For example, having the option to suggest a location or select refreshments makes an employee feel more positive about the meeting. Choices give them the feeling of control. This is also true of savings. While a cushion may not offer complete control over a situation, it does give breathing room to keep us from being overwhelmed.

3. Freedom. People with adequate savings have more freedom than those without. Most people have financial responsibilities: debt, family, or other living expenses. Living in this world means we must buy items and look after those in our care, and it costs us something. Notice this article does not say you should never go into debt. For most people, some major purchases are inaccessible without debt, such as a house. But we should avoid debt that could be avoided by having healthy savings. U.S. credit card debt reached $1.14 trillion in the second quarter of 2024.

This is up 5.8% from the previous year, with the average individual balance hovering around $6,300. Around 60% of people with credit card debt have had it for over a year. Individuals with savings feel less burdened by debt. When you are burdened by debt, you pay out of your income for the principle, interest, and fees on that debt. Having savings and reduced debt allows you to make better use of your income. Also, the weight of debt is great. Romans 13:8 instructs us not to owe anyone anything, except to love each other. The additional weight of debt causes stress that is neither needed nor helpful.

4. Increased self-discipline. Saving money instead of spending it is not easy. If it were, there would be no debt, and people would have no need for financial advisors (or articles like this one). But a savings habit doesn’t have to be a power of will every second of every day. Auto contributions or distributions from your paycheck into a savings account for each pay period can be completed through just a few clicks. And although you are using these tools, you still receive the benefits of self-discipline. Once the funds are separated from your daily accounts, it becomes easier to resist using them, since they are already held in savings. This self-discipline can expand into other areas.

The psychological inertia that initially keeps you from saving works in your favor once you start saving through automatic deposit or transfer. Reducing the number of daily financial decisions has a positive effect on your psyche.

5. Improved feelings of happiness and satisfaction. This psychological advantage leads to improved relationships and a positive outlook. While finances are not the leading cause of divorce in the U.S., stress from money regularly lists among the top reasons cited when filing for divorce. Stress over finances strains relationships, not only with spouses but with friends and family as well. In today’s environment, we constantly compare our lives with those around us. The “bandwagon effect” is a psychological phenomenon in which an individual does something because others, particularly a large group, are doing it. The bandwagon effect causes us to act or behave like others, even when the actions go against our personal beliefs or are ill-advised. Many people become concerned with “keeping up with the Joneses,” which leads to anxiety and depression.

When savings are set aside and our financial house is in order, we reduce anxiety and depression and increase happiness, satisfaction, and contentment with our lives. While we can still fall prey to the bandwagon effect, having savings and reserves that increase each pay period allows us options for better decision-making, keeps us from adding unnecessary debt, and reduces strain on our relationships and families.

Saving provides far more than just financial benefits. It impacts our psychological well-being, a crucial aspect of mental health. Our mental health guides our sense of purpose and helps us cope with the challenges of daily life.

God created us with complex, beautiful emotions and mental capacities. Limiting stress helps us remain healthy and function to the fullest. Small changes in how we spend and save can help provide, protect, and keep us functioning in what God has called us to do.

About the Writer: John Brummitt became director of Richland Ave Financial in January 2016. He graduated in 2011 with an MBA from Tennessee Tech University. A 2004 graduate of Welch College, he has been with Richland Ave Financial since spring 2006. Learn more about retirement options: www.RichlandAveFinancial.com.